Exploring the world of commercial auto insurance for businesses, this guide aims to shed light on the importance of protecting your company vehicles. From understanding coverage options to factors influencing costs, this overview will equip you with the knowledge needed to make informed decisions for your business.

Overview of Commercial Auto Insurance

Commercial auto insurance is a type of insurance policy designed to protect businesses that use vehicles for work purposes. It provides coverage for vehicles used in the course of business operations, offering financial protection in case of accidents, theft, or other damages.

Types of Vehicles Covered

- Commercial Vehicles: Includes trucks, vans, and cars used for business purposes.

- Specialized Vehicles: Such as food trucks, tow trucks, or construction vehicles.

- Employee Vehicles: If employees use their own vehicles for work-related tasks.

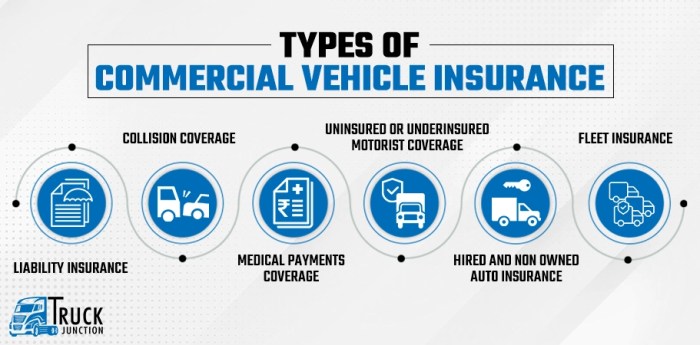

Coverage Options

- Liability Coverage: Protects against damages to others in an accident.

- Collision Coverage: Covers repairs or replacement of the insured vehicle in a crash.

- Comprehensive Coverage: Provides protection against theft, vandalism, or natural disasters.

- Uninsured/Underinsured Motorist Coverage: Covers damages caused by drivers without insurance or insufficient coverage.

- Medical Payments Coverage: Pays for medical expenses for injuries sustained in an accident.

Factors Influencing Commercial Auto Insurance Costs

When it comes to commercial auto insurance costs, there are several factors that insurers take into consideration. These factors can greatly impact the premiums a business will pay for coverage. Let’s explore some of the key elements that influence commercial auto insurance costs.

Type of Business

The type of business plays a significant role in determining commercial auto insurance costs. Insurers consider the nature of the business operations, the goods being transported, and the frequency of vehicle use. For example, a delivery service that operates in a busy urban area may face higher risks compared to a landscaping business that operates in a suburban neighborhood.

Number of Vehicles

The number of vehicles a business owns and operates also affects insurance costs. More vehicles mean a higher potential for accidents or claims, which can lead to increased premiums. Insurers assess the size of the fleet and the usage patterns of each vehicle to determine the level of risk involved.

Driving Records

The driving records of employees who operate the commercial vehicles are crucial in determining insurance costs. Insurers look at the driving histories of all drivers to assess their risk levels. A history of accidents or traffic violations can result in higher premiums, as it indicates a greater likelihood of future claims.

Coverage Limits

The coverage limits chosen by a business can impact insurance costs. Higher coverage limits offer more protection but also come with higher premiums. It’s essential for businesses to strike a balance between adequate coverage and affordability when selecting their policy limits.

Location and Industry Risks

The location of a business and the industry it operates in can also influence insurance pricing. Businesses located in areas with high traffic congestion or high crime rates may face higher premiums due to increased risks. Similarly, industries with higher accident rates or specific hazards may be charged more for insurance coverage.

Importance of Comprehensive Coverage for Businesses

When it comes to commercial auto insurance, businesses should seriously consider adding comprehensive coverage to their policies. Comprehensive coverage provides protection against a wide range of risks that can result in significant financial loss for a business.

Protection Against Various Risks

- Comprehensive coverage can protect a business from non-collision incidents such as theft, vandalism, fire, or natural disasters. For example, if a business vehicle is stolen or damaged in a fire, comprehensive coverage can help cover the costs of repair or replacement.

- Having comprehensive coverage can also safeguard a business from financial loss due to damage caused by falling objects or animals. This type of protection is crucial for businesses that operate in areas prone to such risks.

Coverage for Liability and Collision

Comprehensive coverage not only protects a business from non-collision risks but also includes coverage for liability and collision. This means that in the event of an accident where the business vehicle is at fault, comprehensive coverage can help cover the costs of damages to third parties or property.

Peace of Mind and Financial Security

- By having comprehensive coverage, businesses can have peace of mind knowing that they are protected against a wide range of risks that could potentially disrupt their operations.

- Furthermore, comprehensive coverage provides financial security by ensuring that the business does not have to bear the full financial burden of repair or replacement costs in case of unforeseen events.

Understanding Policy Exclusions and Limitations

Commercial auto insurance policies come with certain exclusions and limitations that businesses need to be aware of to ensure they have adequate coverage in place. It is crucial for business owners to understand these aspects to avoid any surprises in the event of a claim.

Common Exclusions in Commercial Auto Insurance Policies

- Intentional acts: Any damage caused intentionally by the policyholder will not be covered.

- Racing or illegal activities: Accidents that occur while engaging in illegal activities or racing are typically excluded.

- Wear and tear: Normal wear and tear on vehicles is not covered by insurance.

- Hired vehicles: Some policies may exclude coverage for vehicles that are rented or leased.

Limitations in Coverage for Certain Situations or Vehicles

- Non-owned vehicles: Coverage for vehicles not owned by the business may have limitations depending on the policy.

- Employee vehicles: If employees use their own vehicles for work purposes, coverage may be limited.

- Specialized vehicles: Certain types of vehicles, such as heavy-duty trucks or specialized equipment, may have limited coverage under a standard policy.

Ensuring Adequate Coverage

- Review your policy: Carefully review your policy documents to understand what is covered and what is excluded.

- Consider endorsements: Endorsements can be added to your policy to provide additional coverage for specific situations or vehicles.

- Work with an agent: An insurance agent can help you navigate policy exclusions and limitations to ensure you have the right coverage for your business needs.

Final Summary

In conclusion, commercial auto insurance is a crucial investment for businesses looking to safeguard their assets on the road. By opting for comprehensive coverage and understanding policy exclusions, you can ensure your company is protected from potential financial risks. Make the right choice for your business today and drive with confidence.

{kind=link}