Exploring the realm of cheap business insurance for startups, this guide aims to shed light on the importance of insurance for new businesses and how it can be cost-effective. Dive into the world of insurance tailored for startups as we uncover key insights and practical tips.

Understanding Business Insurance

Business insurance is a crucial financial tool that helps protect startups from various risks and uncertainties. It provides coverage for potential losses related to property damage, liability claims, employee injuries, and more. Having the right insurance in place can help startups navigate unexpected events and ensure business continuity.

Types of Business Insurance for Startups

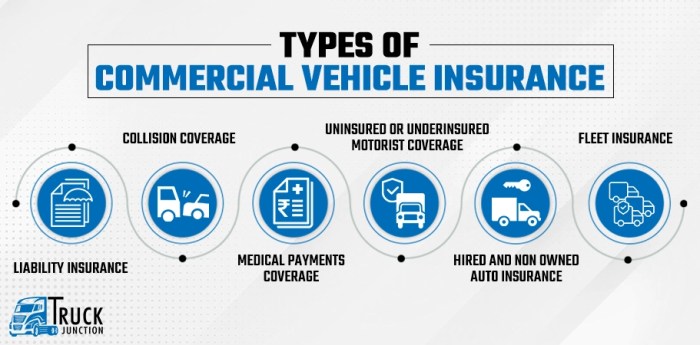

- General Liability Insurance: Protects against third-party claims of bodily injury, property damage, and advertising mistakes.

- Property Insurance: Covers damage or loss of physical assets such as buildings, equipment, and inventory.

- Professional Liability Insurance: Also known as errors and omissions insurance, it safeguards against claims of negligence or inadequate work.

- Workers’ Compensation Insurance: Compensates employees for work-related injuries or illnesses.

Risks Mitigated by Business Insurance

Business insurance can help mitigate risks such as financial losses, lawsuits, property damage, and disruptions to operations. By transferring these risks to an insurance provider, startups can focus on growing their business without constant worry about unforeseen challenges.

Scenarios Benefiting from Business Insurance

- If a customer slips and falls in your store, general liability insurance can cover medical expenses and legal fees.

- In the event of a fire damaging your office space, property insurance can help replace or repair the damaged assets.

- If a client accuses your startup of professional negligence, professional liability insurance can cover legal defense costs and settlements.

Factors Affecting Insurance Costs

When it comes to determining the cost of business insurance for startups, several factors come into play. Understanding these factors can help entrepreneurs make informed decisions to manage their insurance expenses effectively.

Industry Variation in Insurance Needs and Costs

Different industries have varying insurance needs and costs based on the risks associated with their operations. For example, a technology startup may require more coverage for intellectual property protection, while a construction startup may need higher liability coverage due to the physical nature of the work.

- Technology startups may face higher premiums due to the potential for cyber attacks and data breaches.

- Retail startups may need coverage for inventory loss and liability claims from customers.

- Healthcare startups may require specialized coverage for malpractice claims and regulatory compliance.

Impact of Location on Insurance Premiums

The location of a startup can significantly impact insurance premiums. Urban areas with higher crime rates or environmental risks may lead to higher insurance costs compared to rural areas with lower risks. Insurance providers also consider factors like local regulations and weather patterns when calculating premiums.

Startups located in regions prone to natural disasters, such as hurricanes or earthquakes, may face higher property insurance rates.

Tips to Reduce Insurance Costs for Startups

There are strategies that startups can implement to potentially lower their insurance costs:

- Bundle Policies: Combining multiple insurance coverages with the same provider can lead to discounts.

- Implement Risk Management Practices: By minimizing risks through safety protocols and training, startups can demonstrate lower risk to insurers.

- Shop Around: Compare quotes from different insurance companies to find the most competitive rates for your specific needs.

- Consider Deductibles: Opting for higher deductibles can lower premium costs, but startups should ensure they can afford the out-of-pocket expenses if a claim arises.

Researching Insurance Providers

When it comes to finding the right insurance provider for your startup, there are several key criteria to consider. It’s crucial to assess the financial stability and reputation of insurance companies, as well as to obtain quotes from multiple providers to compare policies effectively.

Financial Stability and Reputation

It is essential for startups to research the financial stability and reputation of insurance companies before making a decision. A financially stable insurer is more likely to honor claims and provide long-term support. Checking the reputation through online reviews and ratings can give you insights into the customer service and claim process of the insurance provider.

Obtaining Quotes

Startups should request quotes from multiple insurance providers to compare coverage options and costs. This process involves providing detailed information about your business to each insurer to receive accurate quotes. It’s important to ensure that the quotes are based on similar coverage limits and deductibles for a fair comparison.

Evaluating and Comparing Policies

When evaluating insurance policies from different providers, startups should consider factors such as coverage limits, deductibles, exclusions, and endorsements. It’s crucial to understand the terms and conditions of each policy to determine which one best meets your business needs. Comparing premiums and coverage details side by side can help you make an informed decision.

Tailoring Insurance Coverage for Startups

When it comes to insurance coverage for startups, one size does not fit all. Startups have unique risks and needs that may require customized insurance solutions to adequately protect their business.

Optional Coverage for Startups

- Cyber Liability Insurance: In the digital age, protecting sensitive data and guarding against cyber threats is crucial for startups.

- Professional Liability Insurance: Also known as errors and omissions insurance, this coverage can protect your startup from claims of negligence or inadequate work.

- Business Interruption Insurance: This coverage can help cover lost income and expenses if your startup is unable to operate due to a covered event.

Reviewing and Updating Coverage

It’s essential for startups to regularly review and update their insurance coverage as their business grows and evolves. As your startup expands, your insurance needs may change, so it’s important to ensure that your coverage remains adequate to protect your growing business.

Best Practices for Adequate Coverage

- Work with an insurance provider that specializes in startup insurance to ensure you have the right coverage for your unique risks.

- Regularly reassess your insurance needs and adjust your coverage accordingly to avoid gaps in protection.

- Consider bundling policies or opting for a business owner’s policy (BOP) to potentially save money on premiums while still getting comprehensive coverage.

Ending Remarks

In conclusion, navigating the landscape of cheap business insurance for startups requires careful consideration and strategic planning. By understanding the nuances of insurance coverage and cost factors, startups can safeguard their ventures while optimizing their financial resources.

{kind=link}